Differences between adjustable and fixed rate loans

Differences between adjustable and fixed rate loans

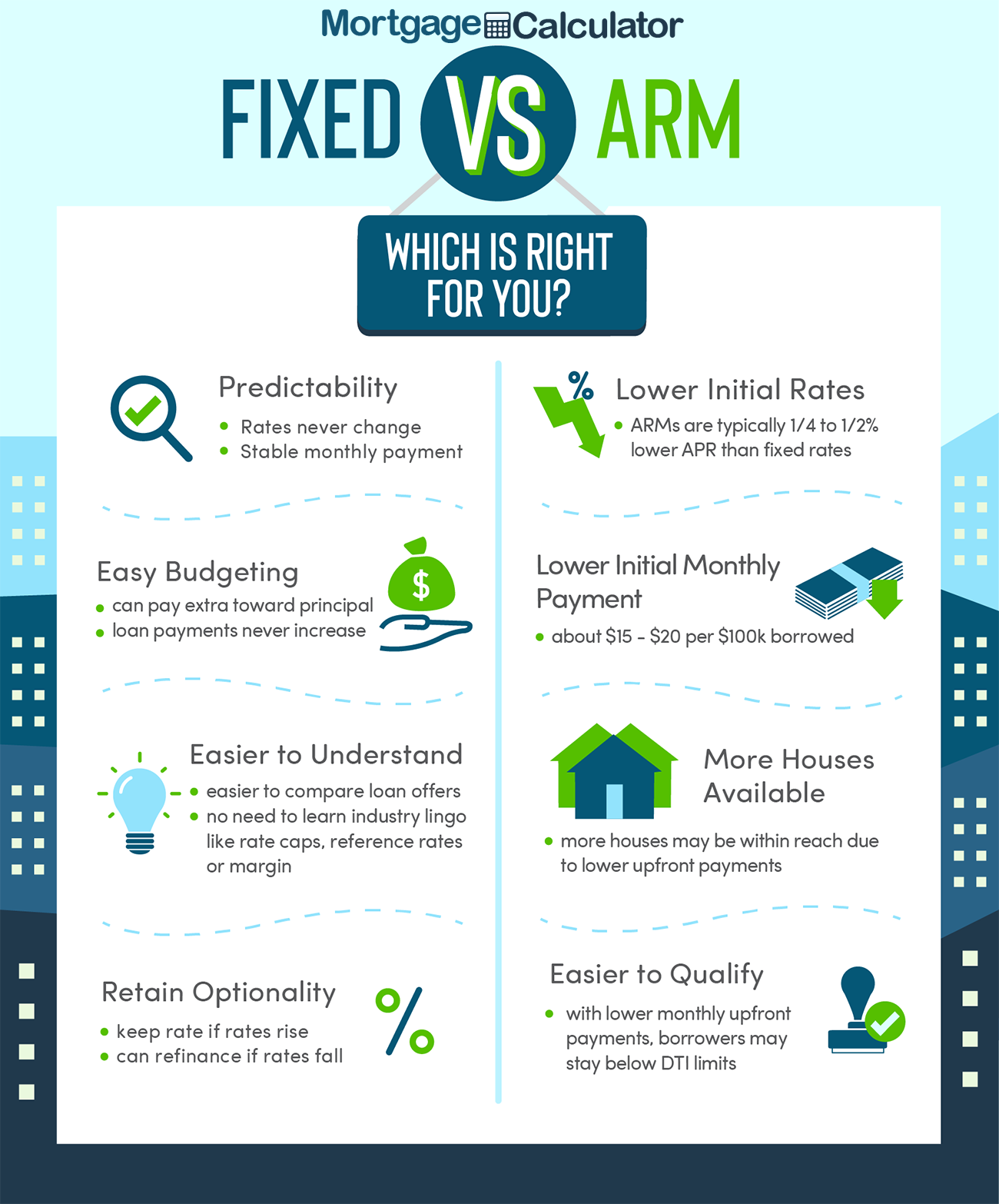

With a fixed-rate loan, your monthly payment stays the same for the entire duration of the loan. The longer you pay, the more of your payment goes toward principal. Your property taxes may go up (or rarely, down), and your insurance rates might vary as well. For the most part monthly payments on a fixed-rate mortgage will increase very little.

Your first few years of payments on a fixed-rate loan are applied mostly to pay interest. That gradually reverses as the loan ages.

You can choose a fixed-rate loan in order to lock in a low interest rate. Borrowers choose these types of loans when interest rates are low and they want to lock in this lower rate. If you have an Adjustable Rate Mortgage (ARM) now, refinancing with a fixed-rate loan can provide greater monthly payment stability. If you currently have an Adjustable Rate Mortgage (ARM), we can assist you in locking a fixed-rate at a good rate. Call Action Mortgage at (713) 723-7800 to learn more.

There are many kinds of Adjustable Rate Mortgages. ARMs are normally adjusted every year, based on various indexes.

The majority of Adjustable Rate Mortgages feature this cap, which means they can't go up over a certain amount in a given period of time. Some ARMs won't increase more than 2% per year, regardless of the underlying interest rate. Sometimes an ARM features a "payment cap" which ensures your payment will not go above a fixed amount in a given year. Plus, the great majority of ARMs have a "lifetime cap" — this means that your interest rate can't ever exceed the capped percentage.

ARMs most often have their lowest rates toward the beginning of the loan. They usually guarantee that interest rate for an initial period that varies greatly. You may have heard about "3/1 ARMs" or "5/1 ARMs". In these loans, the initial rate is fixed for three or five years. It then adjusts every year. These types of loans are fixed for 3 or 5 years, then they adjust. These loans are often best for borrowers who expect to move in three or five years. These types of ARMs most benefit borrowers who will sell their house or refinance before the loan adjusts.

Most borrowers who choose ARMs do so because they want to take advantage of lower introductory rates and don't plan to stay in the house for any longer than the initial low-rate period. ARMs can be risky when property values go down and borrowers cannot sell their home or refinance their loan.

Have questions about mortgage loans? Call us at (713) 723-7800. It's our job to answer these questions and many others, so we're happy to help!